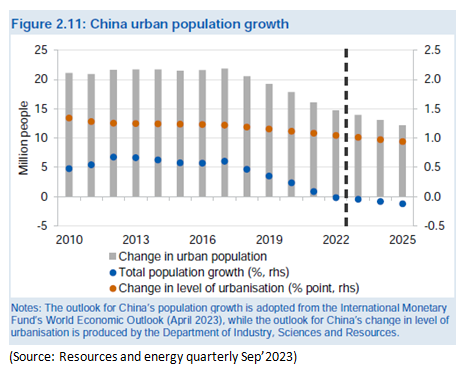

Australian resource and energy commodity prices recorded a further decline in the Sep’2023 quarter, with demand and supply factors mostly pushing prices in the same direction. The Resources and Energy Commodity Price Index fell by 6% (preliminary estimate) in the Sep’2023 quarter to 21% from a year ago in Australian dollar terms. The iron ore price rose in the first half of the Sep’2023 quarter after worries over Chinese demand saw a noticeable decline in Aug'2023 while metallurgical coal prices have edged down as worries over lower demand from Asian steel makers have added to the impact of improving supply. There are rising concerns about economic growth in China. Despite the end of COVID lockdowns, structural and cyclical factors are causing China’s growth to remain relatively weak. While the IMF's core outlook for global growth has improved since June23Q, there is a mounting risk that China’s growth could be weaker than expected largely due to a slowdown in the Chinese property sector. China’s residential property sectors are facing a substantial mismatch in supply and demand due to several demographic and structural factors such as falling population, slowing urbanization, and residential property sales. This could have implications for world commodity markets and Australia as a major supplier of commodities and services to China. China was the largest export market for Australia's resources and energy exports in 2021-22, accounting for more than 35% of export earnings. As such, Chinese demand has a strong influence on commodity prices, so a weaker outlook for Chinese outlook implies weaker Australian export earnings over the long term. (Source: Resources and energy quarterly Sep’2023)

The weaker economic growth outlook in China has led to bouts of weakness in iron ore and base metal prices. However, several stimulus measures announced by the Chinese government and low global inventories for most base metals have helped limit prices to fall further. Spot iron ore prices have been volatile in the Sep’2023 quarter. But, they have generally moderated since the start of 2023 driven by weakness in the Chinese property sector and slowing in global economic growth. Iron ore prices have been volatile in recent months, with prices easing from the end of the June quarter on worries of slowing global economic growth and lower Chinese steel production over the remainder of 2023. Following a strong rebound in iron ore prices to a peak of over US$120 a tonne in the June quarter, the benchmark iron ore spot price (basis 62% Fe fines CFR Qingdao) fell to around US$108 a tonne in August 2023, reflecting slackening demand from Chinese steel mills. Despite the worsening outlook for global steel demand, iron ore prices strengthened again in Sep’2023. The resilience in prices appears to reflect improved market sentiment due to the potential for new government measures to support China’s economy. A substantial level of funding has been allocated for new infrastructures in 2022, as well as new government policies intended to alleviate property sector weakness should provide support for construction activities and hence steel and iron ore demand in China from late 2023 and 2024. Further, the restocking of iron ore and steel inventories by Chinese steel mills is also expected to provide some support for iron ore demand in the coming months.

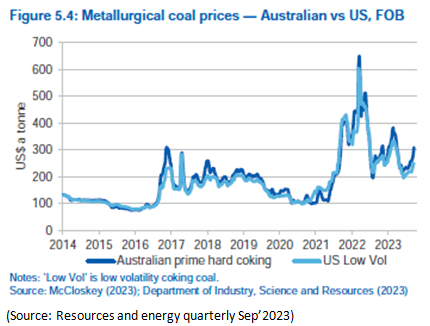

Metallurgical coal prices have remained well above their pre-2019 level, with prices holding up despite a softening global economic outlook. Prices for Australian metallurgical coal are forecast to decrease from US$264 a tonne in 2023 to around US$200 a tonne by 2025. Metallurgical coal prices are expected to edge down over worries of lower demand from Asian steel makers and an improving supply situation in Australia. Most structural factors are pointing towards a softening outlook for metallurgical coal demand. Global steel production is expected to lose some momentum, while supply from Australia is likely to grow following the end of the La Niña cycle. As discussed before, metallurgical coal prices are subject to downside risk arising out of weakness in the Chinese property market. On balance, steadier supply and weaker demand should result in a modest but noticeable decline in metallurgical coal prices, though weather events and conflict around the Black Sea region are likely to add to the upside risks.

After an extraordinary spike in 2022, thermal coal prices fell back sharply in the first half of 2023, but have since stabilized at a relatively strong level. The competitiveness of thermal coal enhanced with the recent increase in gas prices and worries over supply are likely to see Asian stockpiling ahead of the Northern Hemisphere winter to support thermal coal prices in the second half of 2023. However, the outlook for thermal coal looks positive in the near term, growing decarbonization trend to dampen the demand for thermal coal over the longer term. The end of the Northern Hemisphere winter will likely place downward pressure on thermal coal demand from early 2024, and a rise in gas supply should reduce pressure on thermal coal markets from 2025.

AetherReportHub, an authorized representative of AetherSync LLC (LIC No. 2429818.01). Aether Sync has made all efforts to ensure the reliability and accuracy of the views and recommendations expressed in the reports published on its website. Aether Sync's research is based on the information known to us or obtained from various sources that we believe to be reliable and accurate to the best of our knowledge.

Aether Sync provides only general financial information through its website, reports, and newsletters without considering the financial needs or investment objectives of any individual user. We strongly recommend that you seek advice from your financial planner, advisor, or stockbroker regarding the merit of each recommendation before acting on any recommendation based on your own specific financial circumstances. Please understand that not all investments will be suitable for all subscribers.

To the extent permitted by law, Aether Sync Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss, or data corruption). If the law prohibits this exclusion, Aether Sync Ltd hereby limits its liability, to the extent permitted by law, to the resupply of the services.

The securities and financial products we analyze and share information on in our reports may have a product disclosure statement or other offer document associated with them. You should obtain a copy of these before making any decision about acquiring any security or product. You can refer to our Financial Services Guide for more information.