Over the last two years, households and businesses have experienced one thing in common: increasing price levels or inflation. Central banks all over the world have increased interest rates to abate inflation. However, the actions taken by the central banks have significantly slowed down financial activities by reducing the spending power of businesses and households. Lending by banks to households and businesses slowed notably since June 2022 as banks continued to tighten standards and demand for loans softened. Elevated interest rates and rising bond yields are increasing the required cost of capital or discount rate and hence putting upward pressure on equity valuations. There is an inverse relationship between bond yields and stock markets i.e. when yields are rising, stock markets are trending in the opposite direction.

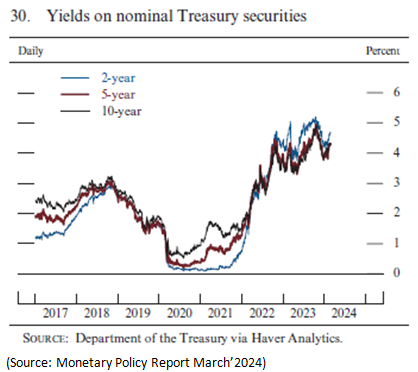

Yields on long-term nominal Treasury securities started to increase in the spring of 2023 and increased markedly through mid-October before reversing course sharply, with the 10-year Treasury yield reaching a peak of about 5% before falling to just below 4% by the end of 2023. So far in 2024, longer-term nominal Treasury yields have increased, with the 10-year Treasury yield rising to about 4.4% by late Feb’2024. The 10-year Treasury yield is considered a risk-free instrument and is closely watched as an indicator of broader investor confidence. Yields on agency mortgage-backed securities (MBS)—an important pricing factor for home mortgage interest rates—increased notably over the summer before falling back down toward the end of 2023. So far in 2024, yields on agency MBS have increased, standing in late February at levels notably above those in June 2023.

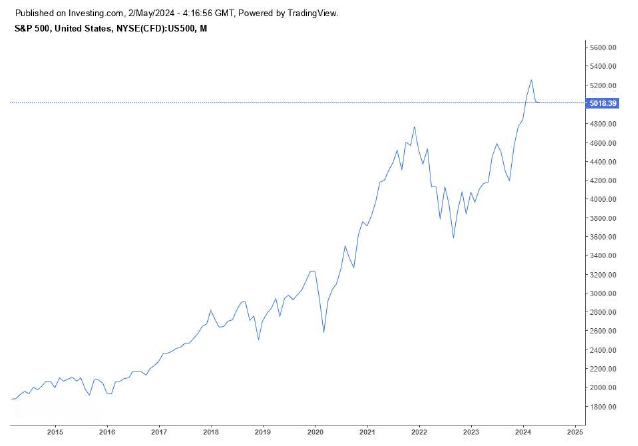

The S&P 500 index which is considered as the best single gauge of large-cap U.S. equities and covers approximately 80% of available market capitalization has increased significantly since June. The S&P 500 index has delivered an annualized price return of 20.78% over the last year to 5035.69 points on 30th April’2024. Following a substantial decline over late summer and early fall, the S&P 500 index recovered toward the end of 2023 with the expectation of rate cuts by the Federal Reserve. The broader equity prices are now at levels close to historical highs, driven mostly by heavyweights such as Microsoft(NASDAQ: MSFT), NVIDIA Corp. (NASDAQ: NVDA), Amazon Inc. (NASDAQ: AMZN), etc. While the broader equity indices performed well over the last year, small-cap indices have underperformed the broader equity indices. The S&P SmallCap 600® index which measures the small-cap segment of the U.S. equity market has delivered a price return of 10.92% over the last year to 1272.36 on 1st May 2024. However, Small-cap companies have experienced an increase in valuations in recent months to the expectations of a less restrictive monetary policy. Banking stocks have retraced some of the declines associated with strains in the banking sector that had occurred over the first half of 2023. In the case of the largest banks, equity prices retraced to their early 2023 levels; however regional bank equity prices experienced only a partial retracement. The VIX which measures the implied volatility of the S&P 500® (SPX) for the next 30 days increased moderately until late October but subsequently declined to reach levels somewhat lower than those prevailing in early June, indicating a bullish sentiment.

In its recent policy meeting concluded on 1 May 2024, the Federal Open Market Committee (FOMC) has maintained interest rates unchanged at 5.25%–5.50%. While inflation has eased substantially over the past year the FOMC cited that there was little progress on its 2 % target inflation and the FOMC is still concerned about inflation risks. The S&P 500 declined 97.78 points to 5018.39 on 1 May 2024 from 5116.17 points on 29 Apr’2024 on the announcement. However, the S&P 500 closed 45.81 points up at 506420. More recently, the rise in consumer confidence with the improvement in real wage prospects offset weakness in the economy amid a higher interest rate environment. We believe that the potential for a prolonged inflation upside and pushing back on rate cuts by the Federal Reserve poses "higher-for-longer" risks that tend to favor value investing strategy vs. growth.

AetherReportHub, an authorized representative of AetherSync LLC (LIC No. 2429818.01). Aether Sync has made all efforts to ensure the reliability and accuracy of the views and recommendations expressed in the reports published on its website. Aether Sync's research is based on the information known to us or obtained from various sources that we believe to be reliable and accurate to the best of our knowledge.

Aether Sync provides only general financial information through its website, reports, and newsletters without considering the financial needs or investment objectives of any individual user. We strongly recommend that you seek advice from your financial planner, advisor, or stockbroker regarding the merit of each recommendation before acting on any recommendation based on your own specific financial circumstances. Please understand that not all investments will be suitable for all subscribers.

To the extent permitted by law, Aether Sync Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss, or data corruption). If the law prohibits this exclusion, Aether Sync Ltd hereby limits its liability, to the extent permitted by law, to the resupply of the services.

The securities and financial products we analyze and share information on in our reports may have a product disclosure statement or other offer document associated with them. You should obtain a copy of these before making any decision about acquiring any security or product. You can refer to our Financial Services Guide for more information.